Tired of Chasing Payments? How Factoring Takes Over Credit Control

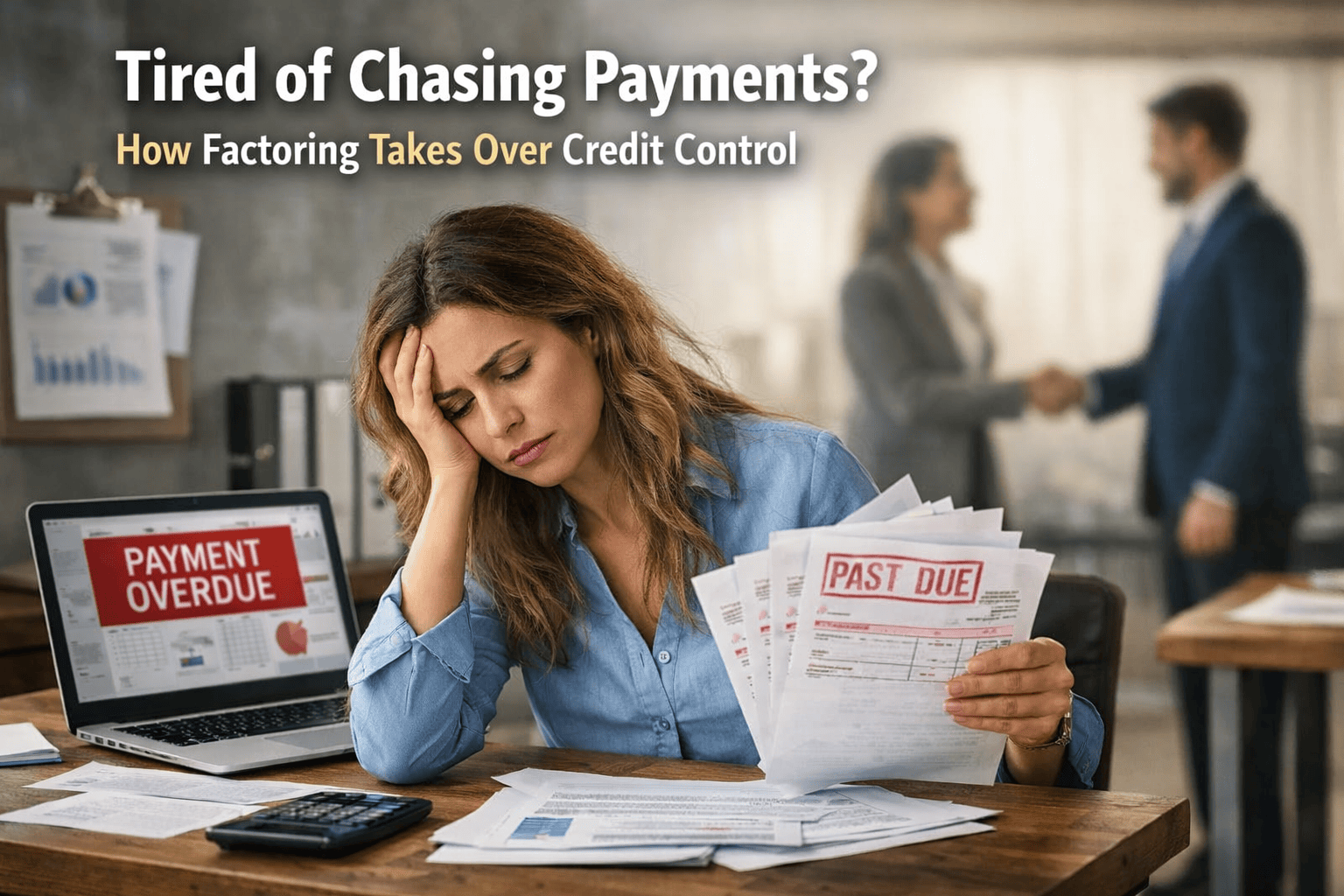

There’s a particular kind of frustration that only business owners understand.

You’ve delivered the work. Sent the invoice. Maybe even followed up politely once or twice. And yet… nothing. Thirty days turns into sixty. Sixty creeps into ninety. Meanwhile, payroll is due, suppliers want paying, and your accountant keeps asking about cash flow forecasts.

Sound familiar?

If you’re running a UK SME or startup, unpaid invoices are not just an inconvenience. They quietly choke growth. And that’s exactly where Factoring steps in.

What Is Factoring and Why Does It Matter?

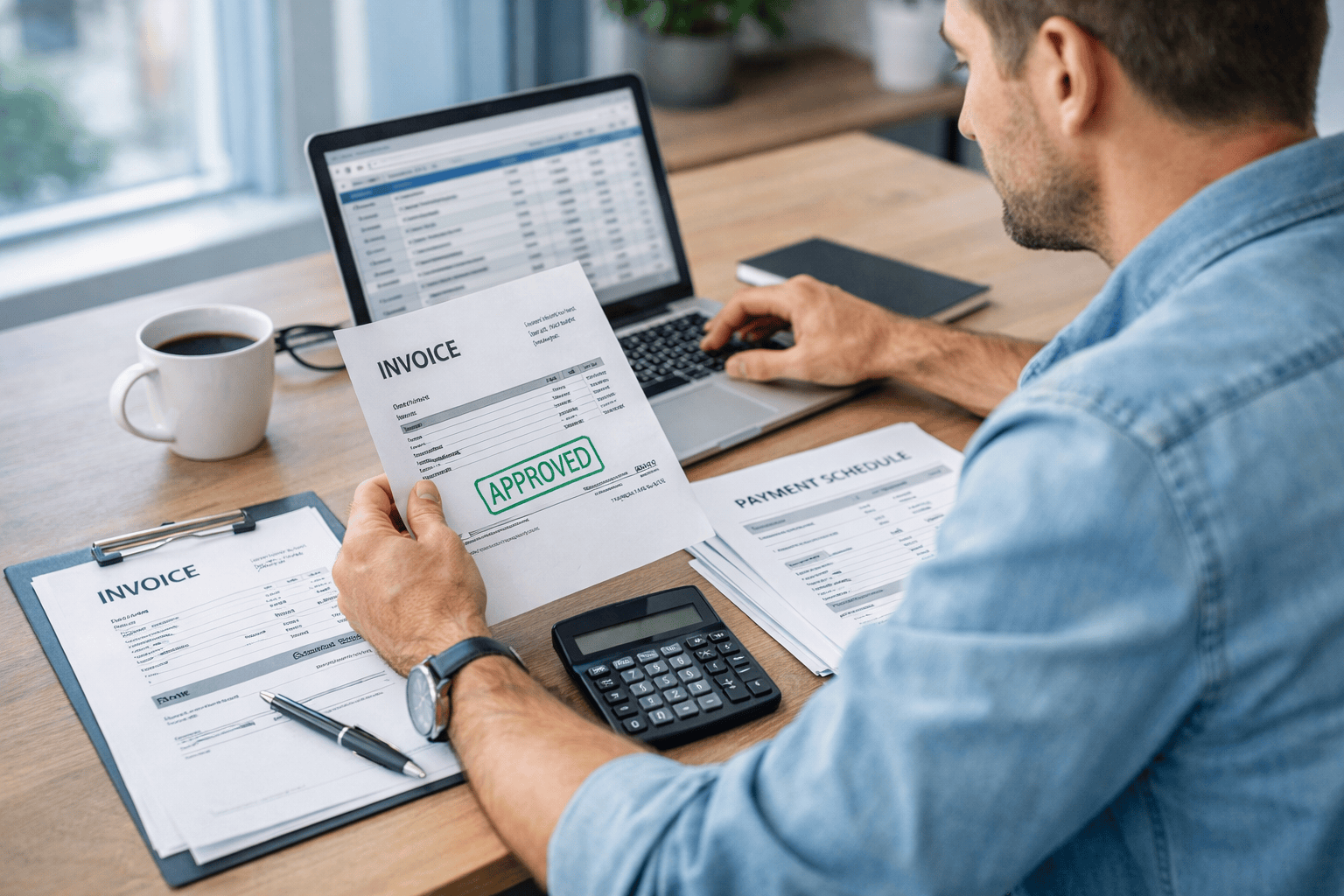

At its core, Factoring is a type of Invoice factoring where you sell your unpaid invoices to a finance provider. In return, you receive most of the invoice value upfront, often within 24 to 48 hours.

But here’s what many business owners overlook.

Factoring does more than unlock cash. It takes over your credit control.

That means fewer awkward phone calls. Fewer reminder emails. Fewer strained client relationships.

You get paid. They chase the debt.

Simple.

The Hidden Cost of Chasing Payments

You probably don’t track how much time you spend on credit control. Most owners don’t.

One late payer might mean three reminder emails, two phone calls, and an uncomfortable conversation. Multiply that by ten clients and you’ve lost hours of productive time. Time that could have been spent winning new contracts or refining operations.

Worse still, chasing debts changes how clients see you. You go from trusted supplier to persistent collector. It’s not a role anyone enjoys.

With Factoring, your provider handles:

- Credit checks on new customers

- Ongoing credit control

- Payment reminders

- Collections

You remain focused on running your business, not policing your cash flow.

How Factoring Improves Cash Flow Immediately

Cash flow is oxygen for growing businesses.

Factoring releases up to 90 percent of your invoice value as soon as it’s raised. Instead of waiting months, you receive working capital almost instantly. That liquidity can cover wages, stock purchases, VAT bills, or investment in new hires.

Unlike traditional loans, Factoring grows with your turnover. The more you invoice, the more funding you unlock. There’s no fixed ceiling that restricts ambition.

It’s one of the reasons many UK SMEs choose Factoring over standard overdrafts or bank loans.

Factoring vs Invoice Discounting: What’s the Difference?

You may also have come across Invoice discounting.

Both are forms of Invoice finance. Both improve cash flow. But they operate slightly differently.

With invoice discounting, you retain control of your credit control and collections. It’s confidential, meaning your customers won’t know you’re using funding.

Factoring, on the other hand, includes outsourced credit control. Your finance partner actively manages your sales ledger.

So which is right for you?

If you’re short on time or struggling with late payments, Factoring often proves more practical. If you have a strong in-house credit control team and prefer discretion, invoice discounting may suit you better.

The decision isn’t about which product is better. It’s about what your business needs right now.

Does Factoring Affect Customer Relationships?

This is a common concern.

Some owners worry that bringing in a third party will damage client trust. In reality, reputable UK factoring providers handle collections professionally and respectfully. They act as an extension of your finance department, not a heavy-handed debt collector.

In many cases, it actually improves relationships. Clear payment processes reduce misunderstandings. Clients know who to pay and when. Communication becomes structured rather than reactive.

And you? You get to focus on delivering value rather than chasing money.

Who Benefits Most from Factoring?

Factoring works particularly well for:

- Recruitment agencies waiting on weekly timesheet payments

- Construction subcontractors with long payment cycles

- Manufacturing firms funding large purchase orders

- Growing startups with limited cash reserves

If your business invoices other businesses on credit terms, Factoring could release trapped capital immediately.

It’s not just about survival. It’s about momentum.

The Emotional Relief You Didn’t Know You Needed

There’s something quietly draining about unpaid invoices sitting on your ledger.

They represent completed work that hasn’t turned into cash. They create uncertainty. They force you into uncomfortable conversations.

When Factoring takes over credit control, that mental weight lifts. You know cash is coming. You know someone else is managing collections. You stop checking your bank balance three times a day.

That clarity allows you to plan with confidence.

And confidence changes everything.

Why Choose Best Factoring?

At Best Factoring, the approach is straightforward. Transparent terms. Flexible facilities. Support tailored to UK SMEs and startups.

No confusing jargon. No rigid structures that box you in.

Whether you need full Invoice Factoring with outsourced credit control or a more discreet Invoice finance solution, the goal remains the same: stronger cash flow and less stress.

If chasing payments has become a weekly ritual you’d rather avoid, it might be time to hand it over.

Ready to Stop Chasing?

Your business deserves predictable cash flow. It deserves your energy directed at growth, not collections.

Explore how Factoring can transform your working capital today at Best Factoring.

Because you built your business to create value, not to chase invoices.

FAQs

1. What is Factoring in simple terms?

Ans. Factoring is a funding solution where you sell unpaid invoices to a finance provider for immediate cash, and they manage credit control on your behalf.

2. How quickly can I receive funds through Factoring?

Ans. Most providers release funds within 24 to 48 hours after you raise an invoice.

3. Is Factoring suitable for startups?

Ans. Yes. Many UK startups use Factoring to stabilise cash flow while growing their customer base.

4. Will my customers know I’m using Factoring?

Ans. In standard Invoice Factoring, customers are aware as payments go to the factoring company. If confidentiality is important, invoice discounting may be an alternative.

5. How is Factoring different from a bank loan?

Ans. Factoring is linked to your invoices and grows with your sales. A bank loan provides a fixed amount with scheduled repayments, regardless of your turnover.

Discover the Latest Trends

Stay informed with our latest articles and resources.